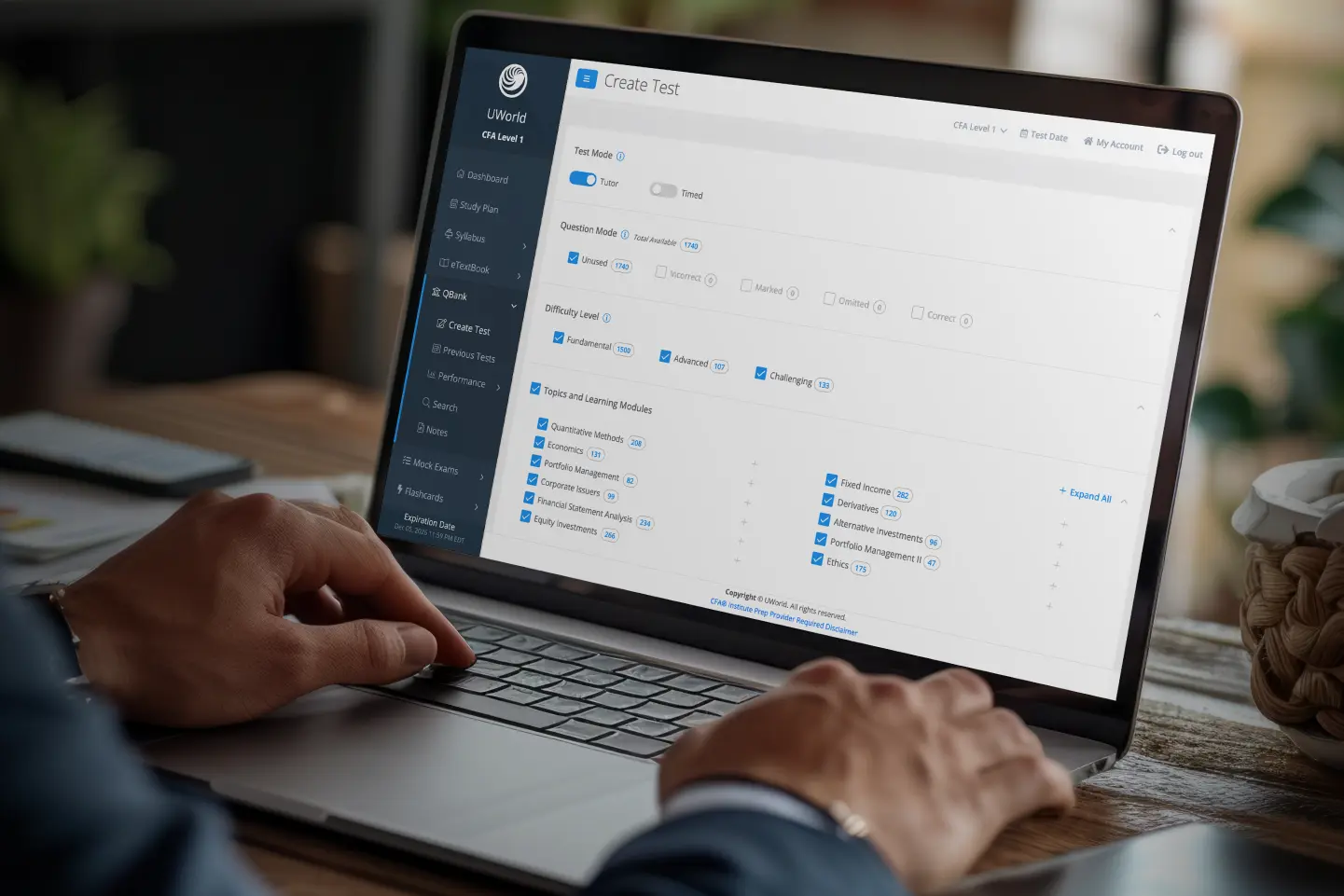

Not all QBanks are created equal. Our high-quality CFA® exam questions and associated rationales will lead you to success. Our CFA questions reflect the latest CFA Institute learning outcome statements (LOS) to ensure you practice everything the candidates are expected to know.

Our CFA exam questions and answer explanations prepared by practicing CFA charterholders with industry and educational experience, mirrors all exam question types and teaches crucial CFA concepts.

Our learn-by-doing philosophy is paired with industry-leading illustrations to help you retain more information in less time

Try it yourself to know what value add you can get from our CFA sample questions and explanations. Furthermore, a complete rationale will be displayed once you submit your answer.

The CFA Level 1 exam is conducted in two sessions with 180 questions in total (90 questions per session) asked in a Multiple-Choice Question (MCQ) format. The Level 1 exam tests your knowledge of different financial concepts, definitions, models, and theorems, your understanding of establishing the connections between concepts, and your ability to think logically.

Select a Question sample.

Select a Question sample.

Compare our Content with our competitors.

According to the Modigliani-Miller propositions (with taxes), if a company increases its debt level, its market value will most likely:

The Modigliani-Miller (MM) propositions assume perfect capital markets (ie, no arbitrage, no transaction or bankruptcy costs, and symmetric information) and assert that a company’s market value equals the present value of its future cash flows. Modigliani and Miller propose that, in the absence of taxes:

However, these propositions change when there are corporate taxes:

Therefore, with taxes, an increase in debt will proportionally increase a company’s value and reduce its WACC.

(Choice A) The MM propositions assume no cost of financial distress.

(Choice B) The market value would remain the same in the absence of taxes.

Things to remember:

The Modigliani-Miller (MM) propositions assume perfect capital markets (ie, no arbitrage, no transaction or bankruptcy costs, and symmetric information). When these propositions include corporate taxes, greater leverage will increase a company’s market value (MM I) and reduce its WACC (MM II).

If a professional organization has standards of conduct in addition to its code of ethics, the purpose of the standards is most likely to describe:

| Instruments for compliance with professional ethics | ||

|---|---|---|

| Instrument | Owner | Describes |

| Code of ethics | Professional organization | Shared principles |

| Standards of conduct | Professional organization | Minimally acceptable behavior |

| Laws and regulations | Government | Legal limits of behavior |

A code of ethics is a professional organization’s statement of shared principles. Standards of conduct provide a guide to practicing the principles outlined in the code of ethics. Standards of conduct also clarify the minimally acceptable behaviors required to conform to the code of ethics. Although not addressed directly in standards of conduct, adherence to civil laws and regulations may be the minimally acceptable behavior in some cases.

Standards of conduct may be principle-based or rule-based. Principle-based standards are universally applicable to members of the profession and are based on the principles outlined in the code of ethics. Rule-based standards, while also relating to the principles in the code of ethics, are usually more narrowly applicable and specific to certain members or scenarios that may arise.

A code of ethics may or may not be accompanied by standards of conduct whereas standards of conduct exist only to enhance their associated code of ethics. CFA Institute has adopted both a code of ethics and standards of conduct (the “Code and Standards”); CFA charterholders and candidates are expected to know and comply with both.

(Choice A) Standards of conduct are used to describe minimally acceptable behaviors or practices, given the shared principles of the code of ethics. The code of ethics describes the shared principles.

(Choice B) Standards of conduct do not describe civil laws and regulations.

Things to remember:

Standards of conduct are used to clarify the minimally acceptable behaviors required to conform to the shared principles stated in a code of ethics; they do not address applicable civil laws and regulations.

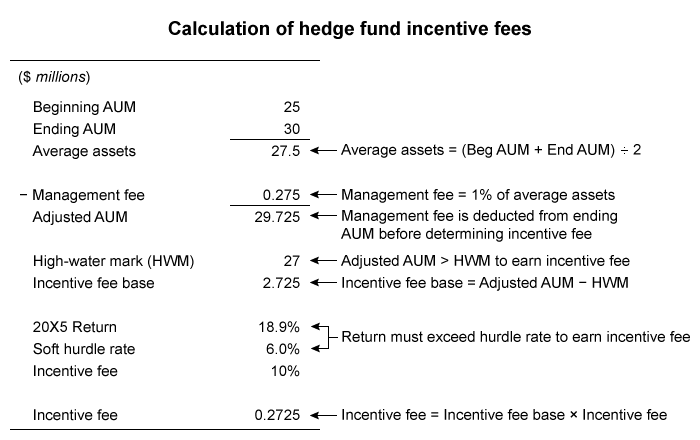

At the end of 20X4, a hedge fund had $25 million in assets under management (AUM). The fund has the following fee structure, high-water mark, and 20X5 results:

| Selected Data | |

| Management fee (average assets) | 1% |

| Incentive fee (net of management fee) | 10% |

| Soft hurdle rate | 6% |

| High-water mark (millions) | $27 |

| Year-end fund assets 20X5 (millions) | $30 |

Assuming no inflows or outflows, the incentive fee (in $) earned by this hedge fund for 20X5 is closest to:

Hedge funds charge a management fee and an incentive fee. The management fee is calculated as a percentage of the total value of the fund’s assets under management (AUM). It is assessed each year regardless of profitability.

The incentive fee is levied against the fund’s annual gains, subject to certain conditions. It is calculated either gross or net of the management fee. The net calculation subtracts the management fee from AUM to arrive at an adjusted AUM that is used to calculate the fund’s profits.

The high-water mark represents the value of AUM, net of fees, at any time during the fund’s existence. To earn an incentive fee, the fund must exceed the high-water mark, the base from which the fee is calculated.

The hurdle rate is the minimum profit that the fund must earn (usually annually) before it receives an incentive fee. The hurdle rate can either be “soft,” meaning that the incentive fee is calculated based on the entire profit, or “hard,” meaning that the incentive fee is based on only the excess profit above the hurdle rate.

In this scenario, the fund generated net returns in 20X5 of 18.9% ( = (29.725 – 25) / 25 ), above the soft hurdle rate of 6%, and eclipsed the high-water mark of $27 million. Therefore, the fund earned an incentive fee of 10% of profits, net of the management fee on average assets of $27,500,000:

0.10 × (29,725,000 − 27,000,000) = $272,500.

(Choice A) $109,000 is the result of incorrectly assuming a hard hurdle rate is in effect.

(Choice C) $300,000 is the incentive fee if management fees are not deducted.

Things to remember:

Hedge funds charge both a fixed management fee and a variable incentive fee. The incentive fee is contingent on whether the fund earns a profit and may be subject to a high-water mark and hurdle rate.

In the short run, a company maximizing profit in a market with perfect competition produces at a quantity that most likely results in:

A firm operating under perfect competition maximizes economic profit by producing and selling at the quantity where marginal revenue (MR) equals marginal cost (MC). Cost in this context includes opportunity costs (eg, the owners’ required return from the business). Perfectly competitive firms can earn economic profits in the short run, but even if economic profits are zero or negative, a firm may be earning an accounting profit.

MR, the incremental revenue from selling one additional unit, depends on the firm’s demand curve. In the case of perfect competition, the demand curve for any individual firm is a horizontal line at the market equilibrium price, since demand is perfectly elastic. Therefore, market price equals MR at all quantities (Choice C).

MC, the incremental cost to produce one additional unit, depends on the firm’s cost structure. Producing at a quantity greater than where MR = MC means that the incremental cost for each unit exceeds the incremental revenue generated by that unit and the firm generates a loss on each additional unit sold. Producing at a lower quantity means that the firm forgoes economic profit (in the short run) since the additional revenue from a unit sold would exceed the cost of the unit.

(Choice A) Perfectly competitive firms can earn economic profits in the short run. However, in the long-run, the positive economic profits will attract new firms, which will increase supply/lower price until economic profit is zero.

Note: Although this question specifically addresses perfect competition, the condition that firms optimally produce when MR = MC applies to all market structures. It is likely that the exam will have questions on this topic.

Things to remember:

Under perfect competition, a firm maximizes short-run economic profit by producing and selling at the quantity where marginal revenue (MR) equals marginal cost (MC). Since there is perfectly elastic demand, price also equals MR for all quantities. Short-run, but not long-run, economic profits are possible. However, a firm may earn an accounting profit even if economic profits are zero or negative.

An analyst observes the following market data for one American put option:

| Selected Data | |

| (in CAD) | |

| Stock price | 48 |

| Strike price | 50 |

| Option premium | 4 |

This option’s moneyness is best described as:

Moneyness refers to the relationship between an option’s strike price and the underlying stock price and is indicative of the option’s intrinsic value. An option trading at the money or out of the money has no intrinsic value. An option trading in the money has intrinsic value:

In this scenario, the put option’s underlying stock price is less than its strike price. Therefore, the option is trading in the money. Note that the option’s premium is irrelevant to determining the option’s intrinsic value; it would, however, be relevant to determining the option’s profit at exercise.

(Choice B) If the stock price equals the strike price, the option is trading at the money (ATM). At expiration, an ATM option is economically equivalent to owning the underlying asset.

(Choice C) For a call option, if the stock price is less than the strike price, the option is trading out of the money (OTM) and has no intrinsic value. The same is true for a put option if the stock price is greater than the strike price.

Things to remember:

Moneyness refers to the relationship between an option’s strike price and the underlying stock price. If the stock price equals the strike price, the option is trading at the money. For a call (put) option, if the stock price is greater (less) than the strike price, the option is trading in the money. For a call (put) option, if the stock price is less (greater) than the strike price, the option is trading out of the money.

A multivariate distribution:

No Additional context, only the formula for the correct answer. The candidate will need to look up the reading for further clarity on the substance and significance behind the formula.

Typical competitor QBanks (especially when free) are part of a much larger learning system that requires an additional purchase for clarity. A multivariate distribution specifies the probabilities for a group of related random variables.

The following data points are observed returns.

14.4%, 17.0%, 19.0%, 22.5%, 4.2%, 6.8%, 7.0%, 10.9%, 11.6%, What return lies at the 70th percentile (70% of returns lie below this return)?

No Additional context, only the formula for the correct answer. The candidate will need to look up the reading for further clarity on the substance and significance behind the formula.

Typical competitor QBanks (especially when free) are part of a much larger learning system that requires an additional purchase for clarity. With 9 observations, the location of the 70th percentile is (9 + 1)(70 / 100) = 7. The seventh observation in ascending order is 17.0%.

The average annual return over 20 years for a sector of mutual funds, calculated for the population of funds in that sector that have 20 years of performance history, is most likely to:

No Additional context, only the formula for the correct answer. The candidate will need to look up the reading for further clarity on the substance and significance behind the formula.

Typical competitor QBanks (especially when free) are part of a much larger learning system that requires an additional purchase for clarity. A sample suffers from survivorship bias if only surviving funds are captured in the data. Funds that cease to exist (due to poor performance) are excluded. This results in an average that overstates the annual return an investor in the sector could actually have expected to earn over the period.

Which of the following statements about a normal distribution is least accurate?

No Additional context, only the formula for the correct answer. The candidate will need to look up the reading for further clarity on the substance and significance behind the formula.

Typical competitor QBanks (especially when free) are part of a much larger learning system that requires an additional purchase for clarity. Even though normal curves have different sizes, they all have identical shape characteristics. The kurtosis for all normal distributions is three; an excess kurtosis of three would indicate a leptokurtic distribution. Both remaining choices are true.

The average return on small stocks over the period 1926-1997 was 17.7%, and the standard deviation of the sample was 33.9%. Assuming returns are normally distributed, the 95% confidence interval for the return on small stocks next year is:

No Additional context, only the formula for the correct answer. The candidate will need to look up the reading for further clarity on the substance and significance behind the formula.

Typical competitor QBanks (especially when free) are part of a much larger learning system that requires an additional purchase for clarity. A 95% confidence interval is ± 1.96 standard deviations from the mean, so 0.177 ± 1.96(0.339) = (–48.7%, 84.1%).

The CFA Level 2 exam has 11 item sets for each session, for a total of 22 on the exam. Multiple-choice questions in each item set must be answered using the information in the vignette. As a result, unlike the CFA Level I exam, the items are not self-contained. The Level 2 exam is essentially a continuation of the concepts covered in the Level 1 exam. The emphasis shifts toward asset classes, though investment tools remain relatively weighted.

Select a Question sample.

Select a Question sample.

Compare our Content with our competitors.

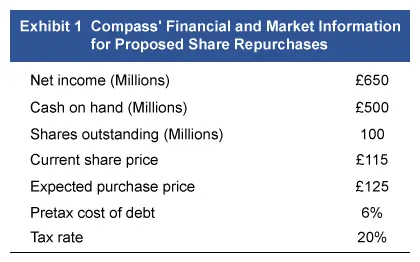

Compass Engineering’s board of directors is deciding between cash dividends or a share repurchase program as a method to begin returning cash to shareholders. Liam Fischer, a member of the board, states that both cash dividends and share repurchases have certain advantages that should be considered:

| Advantage 1: | Share repurchases tend to be more flexible. Although dividends can be raised, lowered, or suspended, they appear to create an expectation among investors that the distribution will continue in the future. Share repurchases do not seem to create the same expectation. |

| Advantage 2: | If the tax rates for capital gains and dividends are the same, and the information content is the same, then shareholders’ wealth will be greater with cash dividends since all shareholders receive cash. |

Alicia Wu, the chairman of the board, indicates that Compass should review the long-term trends in the country (the United Kingdom) before deciding.

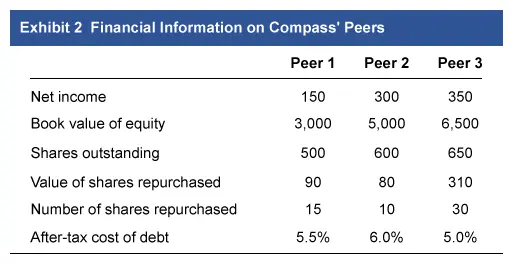

After deliberation, the board favors a share repurchase program. Jessica King, another member of the board, is concerned about the effect of share repurchases on Compass’ EPS. She collects the following data for 20X2:

In addition, King wonders what effect share repurchases have on companies’ book values. She gathers data from three of Compass’ peers who have made a share repurchase:

The board members then discuss the best approach for Compass to repurchase shares. King has identified two possible scenarios, both using the same amount to repurchase shares:

Scenario 1: Purchase shares using all cash on hand.

Scenario 2: Purchase shares with funds from an issuance of debt.

Wu states that her preference is to choose a method by which the company can control the process and execute it quickly. She also prefers a process that would allow Compass to discover the minimum price at which it can repurchase the desired number of shares.

Based on Scenario 1 and Exhibit 1, a share repurchase would cause Compass’ 20X2 EPS to be closest to:

Share repurchases are a popular alternative to cash dividends for returning cash to shareholders. Repurchases allow companies to purchase shares currently being held by shareholders using one of several methods. Once repurchased, the shares are either held for reissue (ie, treasury shares) or retired (ie, canceled shares).

The repurchase leaves fewer shares for investors to hold (ie, shares outstanding), which often results in a change to a company’s per-share financial ratios (eg, EPS). Like dividends, share repurchases are made using corporate cash, whether the cash is on hand or obtained through the issuance of new debt.

In this question, Compass’ EPS following the share repurchase would be £6.77, calculated below.

(Choice A) £6.72 results from incorrectly applying the company’s tax rate to the cash used to repurchase shares, arriving at cash of £400 million [£500 million × (1 − 0.2)].

(Choice C) £6.80 incorrectly uses the company’s share price instead of the purchase price to calculate the number of shares repurchased. Companies do not always repurchase shares at the market price.

Things to remember:

Share repurchases are a popular alternative to cash dividends. They often result in a change to a company’s per-share financial ratios. When cash on hand is used for a repurchase, EPS will always increase. When new debt is issued instead, the change in EPS depends on a company’s after-tax cost of debt and its earnings yield.

Tom Johnson, CFA, is a portfolio manager at Universal Advisors, a US-based wealth management firm that serves high-net-worth individuals and families. Universal’s equity portfolio offering includes separately managed accounts (SMAs) in which clients own individual securities. Johnson manages the portfolio with an aggressive high-risk, high-reward strategy, investing mostly in small-cap growth stocks. To reduce transaction costs and to simplify trading and settlement, Universal buys only US-listed securities for client accounts.

Johnson instructs Francois Martin, a CFA Level II candidate and new equity analyst at the firm, to conduct research on Vent Industries, a French wind turbine manufacturer. Vent is dually listed on exchanges in France and in the US. Martin, a French national who recently moved to the US, is already familiar with the company since he has been following it personally for the past two years.

After completing due diligence on Vent, Martin is thoroughly impressed by the investment prospects and suggests that Johnson add the US-listed shares of Vent to client portfolios. Johnson, as the sole decision-maker, reviews Martin’s research and financial models but wants to think about the suggestion before reaching a conclusion.

Martin is so impressed with Vent’s investment prospects that he wants to buy it for his personal account. For guidance, Martin references Universal’s publicly available personal transaction disclosure, which states only the following:

“Investment personnel are subject to policies and procedures regarding their personal trading.”

Needing more detail, Martin checks with the firm’s compliance officer, who informs him that the firm does have policies and procedures designed to prevent potential conflicts of interest related to personal trading. Universal does not require that employees obtain preclearance before trading, but the firm’s policies do require:

Based on this information, Martin immediately places an order to buy Vent shares listed in France through his personal French brokerage account, which he established prior to joining Universal. Three days later, Johnson decides to invest for clients in the US-listed shares of Vent and places the order through Universal’s trading desk.

Johnson is a board member for a local hospital endowment; for this, he receives modest compensation. Universal has approved Johnson’s board participation and compensation. Johnson is considered to be a thoughtful and successful investor. The other board members, unhappy with the fees and performance of the endowment’s existing income-oriented large-cap equity manager, asked Johnson a year ago if he would be willing to manage the equity portion of the endowment. Johnson responded by stating:

“The hospital provides so much to this community, I would be happy to manage the endowment’s equity portfolio. It won’t even take much time; I will manage the endowment portfolio as an exact replica of Universal’s equity portfolio.”

The next month, without informing Universal, Johnson began managing the endowment portfolio as a mirror image of Universal’s equity strategy.

Recently, Johnson evaluated the investment prospects of an upcoming IPO for a small-cap biotech firm. The company does innovative cancer research, but it is still years away from profitability. After conducting thorough due diligence, Johnson has concluded this is a great investment opportunity; he would like the hospital endowment to participate, believing the other board members would be excited about the company’s cancer research.

Johnson speaks to Universal’s lead underwriter and requests that 5% of the firm’s IPO allotment be allocated to the endowment. A few days later, when the IPO is priced and allocated, Universal receives 95,000 shares and the endowment receives 5,000 shares.

Which of Universal’s procedures for personal investing by employees is inconsistent with CFA Institute’s required and recommended procedures?

“Investment transactions for clients and employers must have priority over investment transactions in which a Member or Candidate is the beneficial owner.”

Standard VI(B) Priority of Transactions stipulates that once a firm has established a policy on personal investing, specific reporting of personal holdings and securities transactions of investment personnel is required to ensure the policy is enforced. Since the policy’s overriding goal is to address client concerns regarding personal securities transactions and any conflicts of interest for the firm’s employees, enforcement procedures must also be established.

Key elements of the enforcement requirements include:

(Choice B) Standard VI(B) stipulates that duplicate transaction confirmations and periodic statements be provided, but it does not specify how frequently. Transaction confirmations should be done at the time of trade to ensure adequate supervision of activity, but quarterly holdings disclosure is adequate and common in most circumstances.

(Choice C) A blackout period is a recommended (not required) policy, and each firm has discretion regarding the period’s duration. Although the minimum period is not specified, a blackout of two days before and after a client trade is likely adequate to minimize market impact and prevent a conflict of interest and/or front-running of client trades.

Things to remember:

The key requirements of Standard VI(B) for investment personnel include trade preclearance and reporting personal holdings and securities transactions.

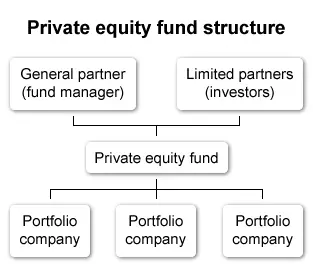

Chao Li is a vice president at Tailwind Capital, a private equity (PE) firm. He is currently raising £100 million for Tailwind Fund A. Li meets with An Heng, an associate at Insular Insurance Co., a potential institutional investor. In their meeting, Li explains the general structure of PE funds to Heng:

Statement 1: The limited partners (LPs) and the general partner (GP) in a private equity fund participate in managing the fund.

Statement 2: The GP is entitled to carried interest, which is typically a percentage of the fund’s profits after management fees.

Statement 3: PE funds are closed-end funds, so LPs can redeem their investments only at specified times.

Heng says, “I understand there are costs associated with investing in PE, such as significant performance fees, dilution costs whenever the PE firm starts new funds, and annual audit costs. And I know that there are some agency risks involved with investing in a PE fund. Is there a governance provision that would address GP gross negligence?”

Subsequently, Li raises the full £100 million for Fund A. One of the fund’s investments is ModernWare, an online services company. The initial investment is £20 million: £13 million in debt, £2 million in preferred equity, and £5 million in the PE fund’s equity. Tailwind plans to sell ModernWare 5 years from now and plans to reduce the debt balance by £10 million by the time of exit. The promised return for the preferred equity holders is 15%.

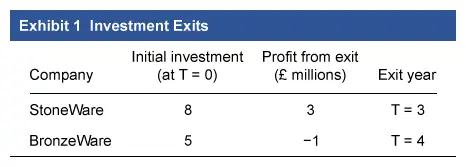

Several years after the fund’s inception, Tailwind exits two investments: StoneWare and BronzeWare (Exhibit 1). Carried interest to the GP is accrued on a deal-by-deal basis and equals 20% of the profits from each exit. The hurdle rate is 10%. When a deal’s IRR is above the hurdle rate, carried interest is accrued; when a deal’s IRR is below the hurdle rate, a clawback penalty amount is accrued if there is a loss.

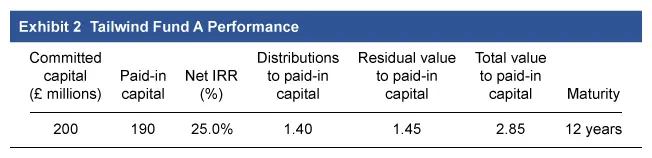

Twelve years after the fund’s inception, Li meets with Heng again to review Fund A’s performance, shown in Exhibit 2.

Which of Li’s statements on Tailwind’s fund structure is incorrect?

Statement 1: The limited partners (LPs) and the general partner (GP) in a private equity fund participate in managing the fund.

Statement 2: The GP is entitled to carried interest, which is typically a percentage of the fund’s profits after management fees.

Statement 3: PE funds are closed-end funds, so LPs can redeem their investments only at specified times.

PE funds are typically structured as limited partnerships in which the GP (ie, fund manager) acts as an agent on behalf of the LPs (ie, investors). The GP actively manages the fund and is responsible for all debts (ie, unlimited liability). The LPs commit capital to the GP, and their liabilities are limited to their invested amounts. Statement 1 is incorrect since LPs are not actively involved in managing the fund.

(Choice B) In exchange for managing funds, GPs charge management fees, some transaction fees, and carried interest.

(Choice C) PE funds are closed-end funds since existing investors are restricted from redeeming their shares for long periods of time. In addition, new investors can be restricted from entering the fund during certain windows.

Things to remember: A private equity fund consists of a general partner (GP) (ie, fund manager) and limited partners (ie, investors). The GP is entitled to management fees and carried interest in exchange for managing the fund. However, the GP is responsible for all the fund’s debt (ie, unlimited liability), whereas the limited partners’ liabilities are limited to their invested amounts.

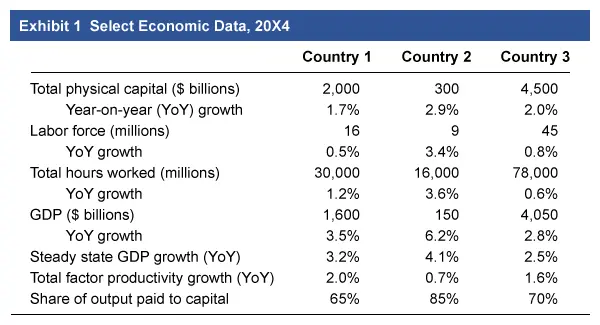

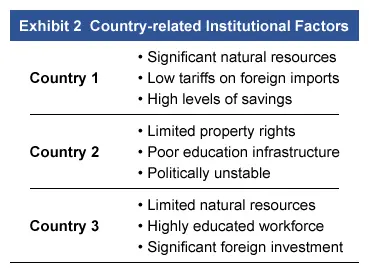

Botan Saito is a portfolio manager for Spire Financial. Spire’s investments are largely domestic, and Saito plans to diversify Spire’s holdings by adding investments in international markets. Saito identifies three countries that he will research further. He collects the following economic data for each country, using average year-on-year growth rates:

During his research, Saito realizes that numbers are not fully explaining the economic differences in these countries. He further researches institutional economic information, shown in Exhibit 2:

Country 2 is planning to implement new policies that create a more open trade policy. Saito expects that this will result in a higher permanent steady-state GDP growth rate.

Saito is interested in how economic factors will ultimately impact each country’s stock market. He notes that Country 3’s:

Saito is also interested in how potential GDP will affect each country’s bonds. He arrives at the following conclusions:

Conclusion 1 Actual GDP growth relative to a country’s potential GDP growth rate is an important factor in central bank decision-making and the likelihood of changes to the central bank’s policies.

Conclusion 2 A decrease in a country’s potential GDP growth rate increases the likelihood that the credit ratings on its sovereign debt will be downgraded.

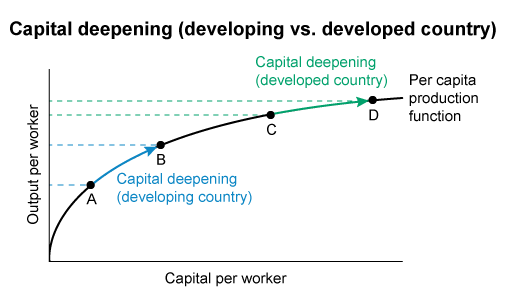

Saito wishes to identify how capital deepening will affect each country’s per capita output growth. Based on the neoclassical model, which of the following factors is most appropriate for Saito to consider?

Capital deepening is an increase in a country’s capital per worker (ie, capital-to-labor ratio). When workers gain more capital, they traditionally become more productive. However, the neoclassical model of economic growth states that the per capita production function, which measures capital per worker against output per worker, exhibits diminishing marginal returns. Therefore, when a country has a greater capital-to-labor ratio, it will likely see a smaller per capita output increase from capital deepening than if it had a lesser capital-to-labor ratio, all else equal.

(Choice B) Steady-state GDP growth considers several factors, including capital growth, labor growth, capital and labor as a percentage of total factor cost, and total factor productivity. Therefore, this measure would not be the most appropriate to identify how capital deepening will affect each country’s growth in output per capita.

(Choice C) Average hours worked per worker affects the factor of labor, not capital, when calculating economic output. Therefore, this measure would not be the most appropriate to use when specifically identifying how capital deepening will affect each country’s growth in output per capita.

Things to remember:

Capital deepening is an increase in a country’s capital per worker. In the neoclassical model, the per capita production function has diminishing returns. Therefore, a country with a greater capital-to-labor ratio will likely see a smaller output increase from capital deepening than a country with a lesser capital-to-labor ratio.

Herman Schmidt is a fund manager working at Rosige Zukunft LLC (RZ), a derivatives trading firm. RZ uses the carry arbitrage model to assess the value of bond forward contracts. Exhibit 1 contains information on several German government bonds that pay coupons once per annum and have five years remaining until maturity. Schmidt directs Hedwig Meyer, an RZ analyst, to price forward contracts on Bond A, Bond B, and Bond C. The 6-month risk-free rate is 1.50% and the 1-year risk-free rate is 2.00%.

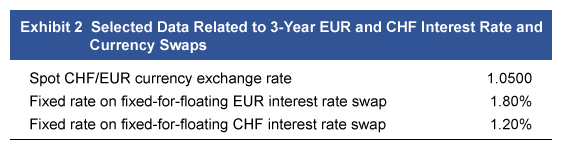

Schmidt and Meyer discuss different methods for valuing interest rate and currency swaps. Exhibit 2 contains information on at-market EUR and CHF interest rate swaps, and the CHF/EUR exchange rate.

Schmidt has RZ initiate a fixed-for-fixed EUR/CHF currency swap, agreeing to pay 1.20% in CHF and receive 1.80% in EUR. RZ exchanges the swap notional with the counterparty at contract initiation, paying EUR 10 million and receiving CHF 10.5 million. Six months later, at-market 2.5-year fixed-for-fixed EUR/CHF currency swaps are quoted at 1.60% EUR for 1.40% CHF and the spot CHF/EUR exchange rate is 1.1000.

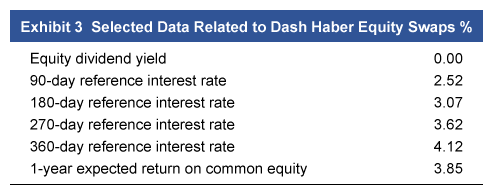

Schmidt anticipates that the equity of Dash Haber Ltd., a UK clothing retailer, will outperform versus expectations. He decides to use a 1-year, quarterly settled, equity-return-for-fixed-interest rate swap to gain long exposure to Dash Haber equity. Exhibit 3 contains information related to the swap:

All interest rates are annual compound rates and are based on a 360-day year.

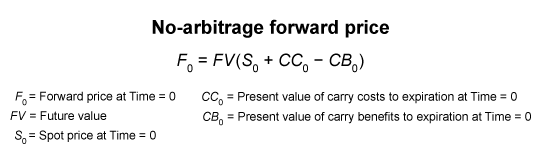

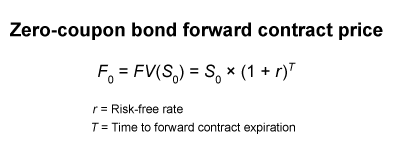

Based on Exhibit 1, the no-arbitrage 6-month forward price of Bond A is most likely:

The no-arbitrage forward price of an asset is the:

The forward price of a zero-coupon bond is just the future value of the bond’s spot price since there are:

As a result, CC0 and CB0 in the formula above both equal 0, reducing the calculation of the no-arbitrage forward price to:

In this scenario, the 6-month forward price of the 5-year zero-coupon bond (ie, Bond A) is calculated as:

If interest rates are positive, the no-arbitrage forward price of an asset with no holding costs or benefits is greater than the asset’s spot price (Choices A and B). The spot/forward price difference reflects the opportunity cost of capital (eg, cost of financing a position in the asset) over the time to the forward contract expiration.

Things to remember:

The no-arbitrage forward price of an asset is the future value of the asset’s spot price adjusted for the costs and benefits of holding the asset to the forward expiration. The forward price of an asset with no holding costs or benefits is above the asset’s spot price by the opportunity cost of capital over the time to the forward expiration.

Tom Harris is undertaking an analysis of the electric scooter industry. He hypothesizes that scooter sales (SALES) are a function of three factors: the population under 20 (POP), the level of disposable income (INCOME), and the number of dollars spent on advertising (ADV). All data are measured in millions of units. Harris gathers data for the last 20 years. Which of the following regression equations correctly represents Harris’ hypothesis?

No Additional context, only the formula for the correct answer. The candidate will need to look up the reading for further clarity on the substance and significance behind the formula.

Typical competitor QBanks (especially when free) are part of a much larger learning system that requires an additional purchase for clarity. SALES is the dependent variable. POP, INCOME, and ADV should be the independent variables (on the right-hand side) of the equation (in any order). Regression equations are additive.

Which of the following statements regarding covariance stationarity is CORRECT?

No Additional context, only the formula for the correct answer. The candidate will need to look up the reading for further clarity on the substance and significance behind the formula.

Typical competitor QBanks (especially when free) are part of a much larger learning system that requires an additional purchase for clarity. Covariance stationarity requires that the expected value and the variance of the time series be constant over time.

The procedure for determining the structure of an autoregressive model is:

No Additional context, only the formula for the correct answer. The candidate will need to look up the reading for further clarity on the substance and significance behind the formula.

Typical competitor QBanks (especially when free) are part of a much larger learning system that requires an additional purchase for clarity. The procedure is iterative: continually test for autocorrelations in the residuals and stop adding lags when the autocorrelations of the residuals are eliminated. Even if several of the residuals exhibit autocorrelation, the lags should be added one at a time.

Tim Watson, CFA, is analyzing sales data for the Tricon Corp, a current equity holding in her portfolio. He observes that sales for Tricon Corp. have grown at a steadily increasing rate over the past ten years due to the successful introduction of some new products. Tim anticipates that Tricon will continue this pattern of success. Which of the following models is most appropriate in her analysis of sales for Tricon Corp?

No Additional context, only the formula for the correct answer. The candidate will need to look up the reading for further clarity on the substance and significance behind the formula.

Typical competitor QBanks (especially when free) are part of a much larger learning system that requires an additional purchase for clarity. The log-linear trend model is the preferred method for a data series that exhibits a trend or for which the residuals are predictable. In this example, sales grew at an exponential, or increasing rate, rather than a steady rate.

Betty Harris, CFA, is considering the purchase of an equity position in Hammer Tech, Inc, a leading seller of hand tools in the United States. Betty has obtained monthly sales data for the past seven years, and has plotted the data points on a graph. She notices that the revenues are growing at approximately 4.5% per year. Which of the following statements regarding Harris’ analysis of the data time series of Hammer Tech’s sales is most accurate? Betty should utilize a:

No Additional context, only the formula for the correct answer. The candidate will need to look up the reading for further clarity on the substance and significance behind the formula.

Typical competitor QBanks (especially when free) are part of a much larger learning system that requires an additional purchase for clarity. A log-linear model is more appropriate when analyzing data that is growing at a compound rate. Sales are a classic example of a type of data series that normally exhibits compound growth.