Accounts payable (AP) is an integral part of any business operations, and efficient management of this process is crucial for maintaining financial stability. However, with an increase in the number of transactions and vendors, managing accounts payable can become a complex task. Therefore, conducting an internal audit of AP is essential to ensure accuracy, completeness, and compliance with regulatory requirements.

Accounts payable internal audit is important for every organization that seeks to maintain financial transparency, accountability, and compliance. The main objective of the audit is to provide assurance to stakeholders that an organization’s business operations, financial systems, and reporting are in compliance with legal regulations, accounting standards, and internal policies.

An internal audit checklist for AP provides a comprehensive framework for conducting a thorough review of the accounts payable process and detecting any potential errors or fraud. In this blog post, we will delve deeper into the importance of an internal audit for accounts payable and the key areas it covers. By the end of this article, you will have a clear understanding of how an accounts payable internal audit checklist can help you identify and mitigate key risks in your AP process.

Internal auditing plays an indispensable role in any organization, ensuring accurate financial reporting, efficient internal controls, and compliance with laws and regulations. It is the backbone of the organization’s governance, risk management, and internal control systems.

An internal accounts payable (AP) audit is a process in which AP internal audit team reviews the accuracy of an organization’s financial transactions. It is conducted to ensure that all payments made to vendors and suppliers are legitimate, accurate, and properly recorded in the books. Through regular audits, the AP team can identify potential risks, irregularities, or loopholes in the financial records, internal controls and operations.

The audit also covers any discrepancies discovered between actual invoices and payments made for them. This particular type of AP audit can provide invaluable insight into an organization’s financial position, allowing stakeholders to make more informed decisions on how best to manage existing resources or determine where additional funds might be needed.

The internal audit process is crucial for improving an organization’s operations and achieving continuous improvement. It helps to identify inefficiencies and weaknesses in internal controls, which can lead to streamlined operations, cost reductions, and improved overall performance.

Without an AP internal audit, organizations would face significant risks such as inaccurate financial reporting, non-compliance with laws and regulations, mismanagement of resources, and potential litigation. The consequences of these risks are not only financial but can also significantly damage the organization’s reputation, trust of stakeholders, and employee morale.

On the financial side of things, the consequences of non-compliance can include fines and legal action. Additionally, regulatory agencies require companies to have effective internal control systems and ensure accurate financial reporting.

In short, the AP internal audit matters because it helps organizations to achieve their objectives, maintain accurate financial reporting, and comply with laws and regulations while mitigating risks associated with operations. It promotes transparency, accountability, and good governance, and is an essential part of any successful organization.

An AP internal audit checklist is designed to provide guidance and structure for the audit team in evaluating the AP function and determining its compliance with the organization’s policies and regulations, industry standards, and legal requirements.

The AP internal audit checklist should cover the four main controls:

Obligations to pay controls is the first line of defense against AP fraud and errors. These controls play a vital role in ensuring that payments are accurately made to the correct vendors or suppliers. There are four essential controls under this category: Purchase Order (PO) approval, Invoice approval, Three-way matching, and Duplicate payment searches.

A purchase order (PO) approval is a process that requires obtaining authorization from the appropriate individual or department before making a purchase. During an internal accounts payable (AP) audit, PO approval is an essential area of review as it helps auditors to determine whether the company’s PO approval process is effective in preventing unauthorized purchases and ensuring that all purchases are necessary and reasonable.

Invoice approval audit involves verifying the accuracy of invoices and ensuring that they are properly authorized for payment, and that the authorization complies with the company’s policies and procedures. The invoice approval process helps ensure that the same person is not responsible for both approving invoices and processing payments, reducing the risk of fraud.

The 3-way matching process typically involves reviewing and comparing the invoice with supporting documents, such as purchase orders, delivery receipts, and contracts, to ensure that the goods or services were received and that the prices and quantities are correct.

Duplicate payment search is a control in the Accounts Payable (AP) process that involves identifying and preventing duplicate payments. Duplicate payments occur when the same invoice is paid twice. The process of duplicate payment search involves reviewing payment records and identifying payments that match in terms of vendor, amount, and invoice number.

Data entry control ensures that all information entered into the system is accurate, complete, and consistent. The accuracy of data entry is vital, as it impacts the validity of financial records and reporting. Inaccurate data can lead to improper payments, fraud, and other financial losses.

To maintain proper data entry control, internal AP auditors must develop and implement effective control procedures. These procedures should include measures to authenticate and verify the accuracy of all data entered into the system. Additionally, internal auditors should conduct periodic reviews to identify any errors or discrepancies.

Payment controls are by far the most critical aspect of any internal AP audit. These controls help ensure that payments are accurate, timely and secure. One key control is segregation of duties, which separates the responsibilities of those who initiate, approve and reconcile payments.

Regular monitoring and analysis of payment data should be conducted to detect any unusual patterns or deviations from established processes. This can include identifying duplicate payments or unapproved vendors.

To further strengthen payment controls, it is important to have a robust system in place for securing payment information and access. This may include password protection, restricted access to payment systems and secure storage of payment data.

One of the primary risks in accounts payable is the potential for fraud in vendor payments. Fraudulent vendors can submit false invoices or inflate prices, causing a significant financial impact to the organization.

To reduce the risk of fraud, internal AP auditors should implement several control measures. Firstly, auditors should conduct thorough assessments of vendor information, including verifying business licenses, tax records, and other documentation.

Secondly, proper authorization procedures should help ensure that false or fraudulent invoices do not get approved. Controls should require sign-offs from multiple individuals for invoices and vendor payments.

Regular monitoring of the payment patterns and account reconciliations is an important control measure. The internal auditors can verify invoice numbers, dates, and amounts paid, and then cross-validate the data with payments made in bank statements. Any discrepancies should be immediately reported and investigated.

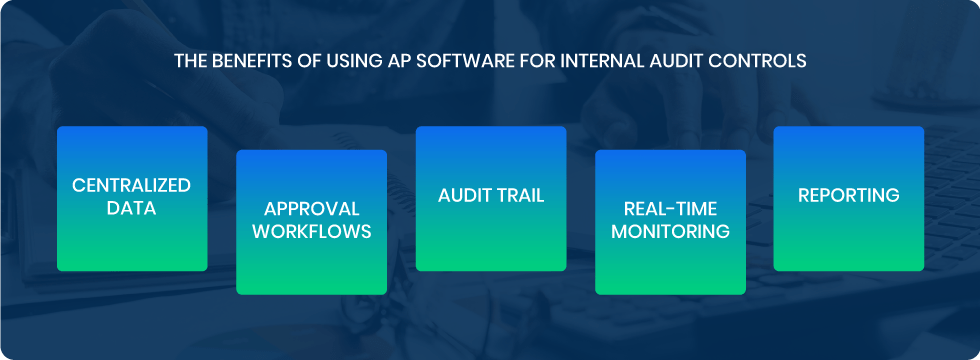

Automating internal audit controls with AP automation software is the perfect way for businesses to stay organized and reduce costs. Instead of manually crossing-checking invoices, purchase orders, approvals and payments, AP teams can use software to detect anomalies, errors and frauds.

Here are some of the perks of using AP automation software to conduct the internal AP audit:

It is generally recommended that internal AP audits be conducted at least once a year to ensure that the organization’s financial records are accurate and up-to-date and that there are no errors or discrepancies in the AP process.

If there has been a change in the organisation’s accounting system or processes, or if there have been significant changes in the environment in which the organisation operates, it may be necessary to conduct an audit more frequently. If there are identified issues with the AP process, like fraud or errors, it may be necessary to conduct an audit immediately to address the issues and prevent their re-occurrence.

One of the biggest advantages of internal audits is that the AP team has an intimate knowledge of the organization’s financial systems and processes. They are better equipped to understand the unique needs and requirements, plus internal audits are typically less expensive than external ones.

However, internal auditors may lack the impartial and objective perspective that an external auditor would bring, and they may also lack the specialized knowledge required to perform complex audits, which could lead to oversights or errors.

External auditors have no prior attachments or loyalties to the organization; they are independent, objective, and impartial, which can provide greater credibility to the audit’s findings. They can also bring a fresh perspective, identify areas for improvement that may have gone unnoticed by an internal team. On the downside, external audits require more time to prepare and achieve, and depending on the scope of the audit, they can be expensive.